The EU's debt rules will be reformed this year. The new rules will affect, for example, the speed and time at which the Member States must reduce their debt ratio. The need for fiscal adjustment, i.e. tax increases and expenditure cuts, is assessed specifically for each Member State by means of the debt sustainability analysis.

Writer

The state of general government finances has been in the headlines frequently in recent months. When the need for further adjustment has been discussed by different actors, the estimates have been in the range of billions of euros.

Differing adjustment estimates are likely to continue, but what is more essential than an exact amount in billions is that the longer-term development of public finances is in the right direction.

It is no surprise that further adjustment is needed. At the end of last year, the fiscal policy monitoring function assessed that achieving the Government’s deficit objective was likely to require additional measures and extending the range of measures.

In other words, the Government’s debt targets and fiscal measures are not in balance. Tax measures are also needed to support major expenditure decisions.

The adjustment debate is centred around the EU fiscal rules. According to them, the general government deficit may not exceed 3% and the debt ratio may not exceed 60% of GDP. In the light of recent forecasts, it seems that, without new adjustment measures, the general government deficit will exceed the 3% reference value in the current and the following year.

Exceeding the reference value may lead to the excessive deficit procedure (EDP), which means that the Member State must adjust its public finances under the supervision of the EU Commission and Council.

The new EU debt rules will set different objectives for the Member States

Less attention in the public debate has been paid to a more significant issue: the ongoing reform of the EU fiscal framework, which is about to be completed. The reform will significantly change the current EU fiscal rules, even though the reference values for the general government deficit and debt ratio, as specified in the Treaty, remain unchanged.

The aim of the reform is to simplify the framework and to take better account of the different fiscal challenges faced by the Member States.

In future, each Member State will negotiate a medium-term fiscal structural plan for itself with the Commission. The plan will describe the measures that the Member State intends to take in order to bend the growth curve of its government debt and to create sustainable growth.

Based on the legislative proposal of the Commission, the Member States reached a compromise on new fiscal rules last December (Opens in a new tab). In chapter 3 of the fiscal policy monitoring report (2023), we analysed the Commission’s legislative proposal and the related debt sustainability analysis in detail.

The EU Council and Parliament also reached agreement in the negotiations early this year (Opens in a new tab). The Member States are now expected to submit their medium-term plans in autumn 2024. The new rules will apply to the fiscal policy for 2025.

In any case, 2024 will be a year of transition from the old rules to the new ones.

Member State-specific assessment is a step in the right direction

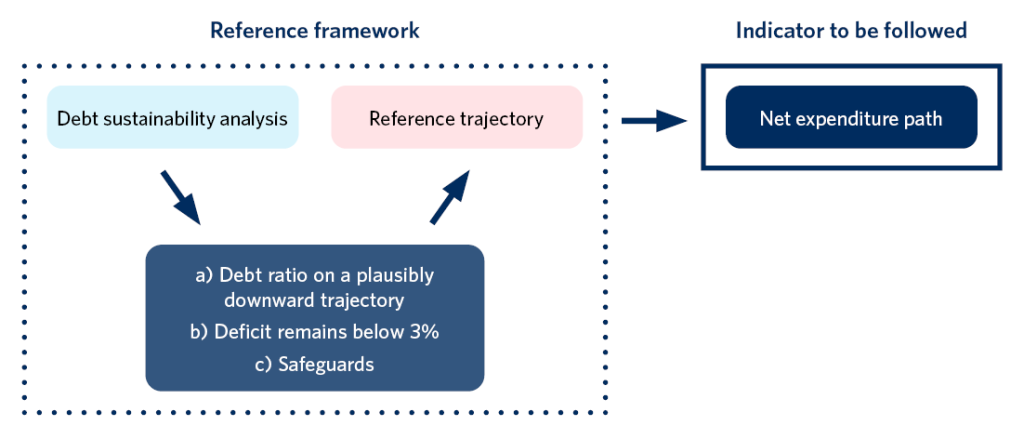

The cornerstone of the reform is the debt sustainability analysis. The debt sustainability analysis provides an estimate of how the deficit and debt ratio will develop based on certain economic growth, interest rate and primary balance forecasts. Any deviations of these variables from their assumed trajectories are also taken into account in the analysis.

By means of the analysis, the Commission calculates for each Member State a ‘reference trajectory’, with which the estimated debt ratio will be on a plausibly downward trajectory in the future. With the reference trajectory, the estimated deficit must also remain below the 3% reference value.

In addition to these criteria, some Member States required additional safeguards in the rules to ensure that the estimated deficit and debt ratio will decrease already during the adjustment period. The safeguards set strict numerical criteria for the deficit and debt ratio, which the reference trajectory must fulfil regardless of the results of the debt sustainability analysis.

In Finland, for example, the debt ratio should decrease by an average of 0.5 percentage points during the adjustment period. This means a decrease of 2 percentage points in the debt ratio during the four-year adjustment period. In addition, to create a safety margin, the structural deficit must be 1.5 percentage points from the 3% reference value.

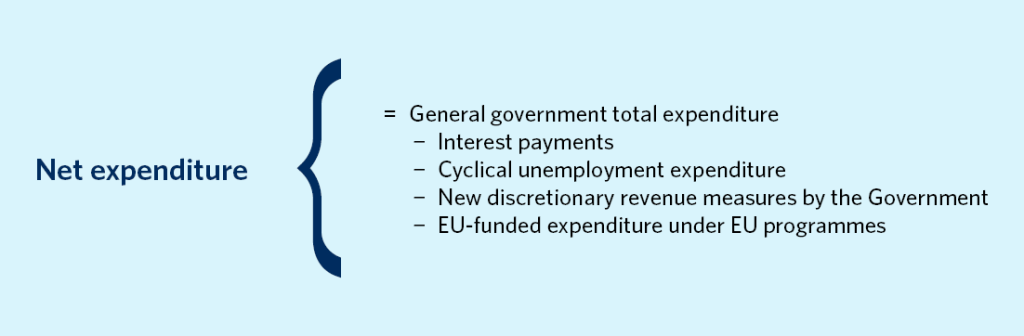

The debt sustainability analysis results in a reference trajectory that meets all the three criteria presented in Figure 1. The criterion that gives the strictest reference trajectory serves as a so-called restrictive criterion. The net expenditure path, defined in Figure 2, is derived from this reference trajectory.

On the basis of the reference trajectory published by it, the Commission will engage in bilateral discussions with each Member State on the fiscal structural plan, fiscal adjustment path, and structural reforms and investments. The final net expenditure path (and the corresponding adjustment path) will be determined after the fiscal structural plan has been assessed (by the European Commission) and approved (by the Council of the European Union).

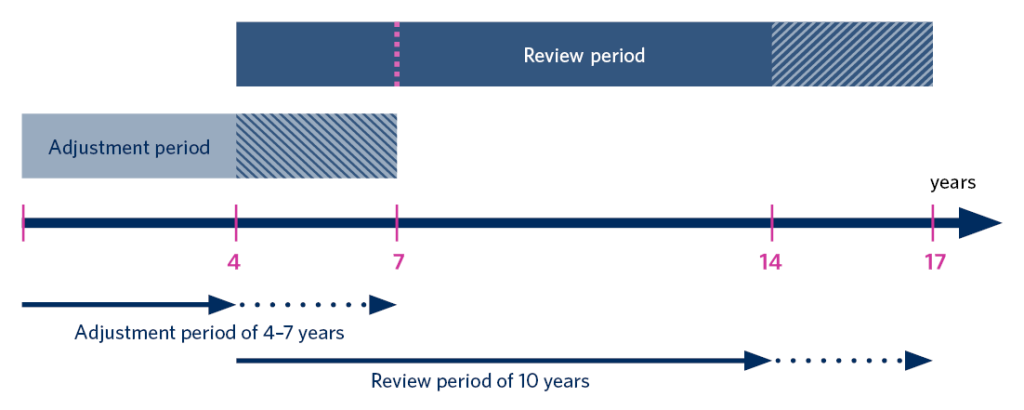

The reference trajectory can be divided into an adjustment period and a review period (Figure 3). The adjustment period is four years. This can be extended by a maximum of three years if the Member State commits itself in its plan to growth-supporting reforms and investments. The review period is 10 years, during which the development of the debt ratio and deficit is assessed.

Debt sustainability analysis aims to identify the main risks affecting debt development

The debt sustainability analysis serves as a useful framework and analysis tool for determining the net expenditure path to be followed by each Member State. The debt sustainability analysis is applied separately to each Member State. The economic growth, interest rate and primary balance forecasts in the analysis are country-specific. However, some of the underlying assumptions in the analysis are the same for all countries.

The analysis also takes into account various economic dependencies, such as the multiplier effects of fiscal policy. This and all other assumptions will be assessed in a specific working group to be set up.

The new debt rules are, in many respects, a compromise. They reflect the clear dividing line that exists between the Member States as regards the role of fiscal policy. However, the reform contains many elements that make it possible to respond to unexpected economic shocks while helping to ensure long-term debt sustainability.