Assessments of the economic impacts of the corona crisis differ considerably from one another. The crisis is hitting particularly hard the service sector, which has provided stability during many previous recessions. It has affected the labour market untypically fast. This is particularly worrying from the perspective of domestic demand. What we need now desperately is such measures to fight the pandemic that would enable the wheels of the economy to turn. This article is part of a series of blog posts dealing with the economic impacts of the coronavirus.

Writers

Matthias Strifler

Senior Economist, PhD

Monitoring and Oversight

Jenni Kellokumpu

Senior Economist, PhD

Monitoring and Oversight

In the public debate, the present economic crisis has been compared to the financial crisis, the recession of the 1990s, the Finnish famine of 1860s, and even the Finnish Civil War. There is a lot of uncertainty as regards how deep the slump will be. The uncertainty is largely due to the lack of information on the spreading and lethality of the coronavirus – and on the duration of the restrictions imposed. In fact, the only thing we know for certain is that a deep crisis is possible.

There is also uncertainty among economic forecasters both in and outside Finland. Instead of economic forecasts, they are now publishing scenario calculations. These calculations aim at giving a true picture of the economy, provided that certain assumptions are realized, such as the assumed spreading speed of the disease and the assumed duration of the restrictions.

Scenario calculations are important, as they reflect what the forecasters consider possible. At present, scenarios on the impacts of the crisis on Finnish GDP vary between –1% and –13%. The range covers almost all options from a slight contraction of GDP to a severe depression.

The situation is the same in other countries, too: scenarios on the change in GDP vary between –2% and –8 % in Sweden, between –2% and –21% in Germany, and between –1% and –12% in the US. Uncertainty in other countries increases the uncertainty about the economic development in Finland, as exports play an important role in our economy.

Early indicators paint a gloomy picture

The so-called early indicators illustrating the economic atmosphere can give some indications of the future economic development. The picture they paint is rather gloomy: the European Commission’s economic indicator for the EU and the euro area, for example, contracted to the same extent as during the financial crisis, even though the indicator surveys were conducted mainly before any restrictions had been imposed in the EU.

The Eurozone Purchasing Managers’ Composite Index of IHS Markit is even more pessimistic and actually collapsed in March. The fall was more dramatic than ever before. The corresponding Global Economy Index has contracted in the same way as during the financial crisis. The surveys related to this index were also conducted partly before any restrictions were announced. According to these indices, the decrease in Finnish GDP in 2020 would be at least in the same ballpark as during the financial crisis and the 1990s recession.

Policy measures are taken exceptionally on two fronts at the same time – to fight against the disease and for the economy

It is difficult to forecast the magnitude of the crisis based on the change in GDP. However, the coronavirus crisis has certain special characteristics, the knowledge of which may facilitate the planning of fiscal policy, which is built on incomplete knowledge. The biggest difference between the current situation and the financial crisis and many other economic crises is that, in the ongoing crisis, the original shock came from outside the economy. When the shock comes from within the economy, fiscal policy has only one goal: fast return to the growth path.

In the present crisis, there are at least two goals: successful fight against the disease and dampening the fall of the economy. Political decisions have slowed down the spreading of the disease, but at the same time, they have also reduced economic activity. Fiscal policy measures, in turn, are taken to mitigate the impacts of the restrictions. The situation is therefore quite exceptional, and there is no ready-made solution.

Although the reasons for the crisis are outside the economy, it should be taken into consideration that multiplier effects may occur within the economy if fiscal policy fails to protect and support businesses during the crisis. Such effects will be seen at the latest if healthy companies start to go under because of lack of liquidity.

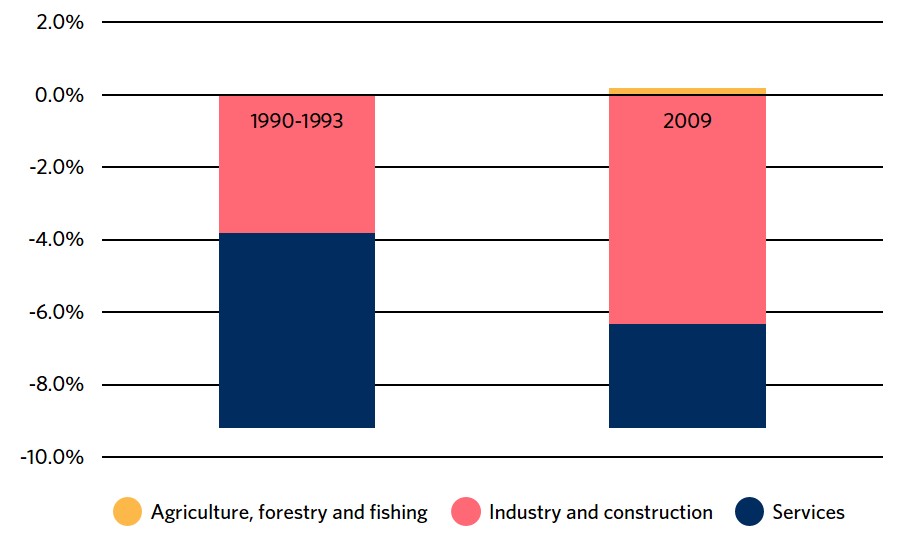

Service sector is a major employer and the biggest sufferers – just like in the recession of the 1990s

Another special characteristic of the present crisis is the key role played by the service sector. During several previous crises, the service sector has acted as a buffer, as it has often remained stable or even grown despite a recession. This time the demand for services is undergoing a free fall, as both the disease and the restrictions imposed hit the service sector particularly hard. The fact that the service sector is a major employer with an especially important role in the labour market makes the problem even more difficult. If the service sector suffers in the same way as in the recession of the 1990s, the economic crisis will deepen and drag on.

The figure below illustrates the share of different sectors in the change in gross value added during the 1990s recession and the financial crisis. The figure shows that, compared with the financial crisis, services employing a large number of people decreased almost twice as much during the 1990s recession. The loss of jobs in the service sector is therefore reflected much more strongly in the employment rate.

Employment also recovers much more slowly in the service sector than in industry – particularly if companies operating in the sector go bankrupt during the crisis and unemployment causes household consumption to remain permanently at a lower level after the crisis. If the ongoing crisis, which affects the service sector in particular, is prolonged, there is a risk that, rather than being a temporary phase that will soon be over like the financial crisis, it will become a period of slow recovery like the 1990s recession.

The special characteristics of the present crisis also include its immediate impact on the labour market. This can already be seen in many countries: the US has a record number of people who have filed for unemployment benefits, Germany has a record number of people with a shortened working week, and Finland has a record number of people who have been laid off or are threatened by layoffs. The number of new unemployed is about 12,000, and the number of laid-off employees is about 85,000. More than 360,000 people are threatened by layoffs.

Usually the labour market follows changes in GDP with a delay, and therefore it is quite exceptional that the labour market now serves as a forerunner and even an early indicator in the crisis. This is an alarming trend, because it will also reduce household consumption. During the financial crisis, for example, household consumption in Finland contracted by about 3%. Even in this respect, the present crisis bears resemblance to the 1990s recession, during which consumption contracted much more drastically, by about 10%.

It is necessary to link defending the economy with fighting the coronavirus

Finland is unable to influence the development of the global economy and exports. We can, nevertheless, influence domestic demand and the operation of the Finnish service sector. The restrictions imposed play a key role in this. As the situation may drag on, it is of utmost importance to find measures and means that enable both business and successful fight against the disease. Many countries in Europe – e.g. Austria, Denmark, and our neighbour Norway – are already heading in this direction.