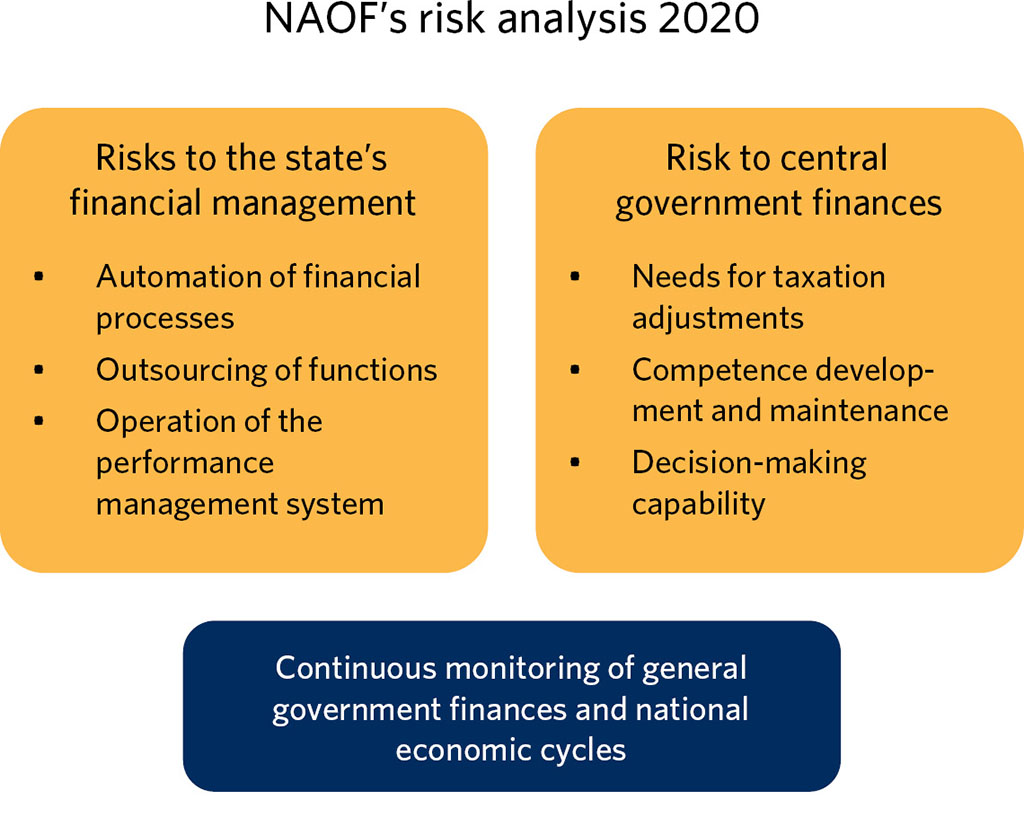

The National Audit Office of Finland (NAOF) has identified such key risks to the state's financial management and central government finances in the years to come as can be impacted by auditing. The NAOF's risk analysis supports both the planning of audits and the audited entities’ own risk management. Based on its own audit work, the NAOF identified the following as the key risks to central government finances: automation of financial processes, outsourcing of functions, and operation of the performance management system. The risks related to central government finances, in turn, were identified by analysing the vision of the future laid out by the Prime Minister's Office. The NAOF has assessed the vision of the future particularly from the perspective of future development of central government finances and the impact of audits. The following risks were identified: needs for taxation adjustments, competence development and maintenance, and decision-making capability.

To support the planning of audit work, the National Audit Office of Finland (NAOF) makes a risk analysis. The NAOF’s risk analysis can also support the audited entities’ risk management. The issues that are identified and selected are estimated to be the most relevant to the state’s successful financial management and sustainable central government finances in the future.

The analysis compiles such key risks to the state’s financial management and central government finances as can be influenced by auditing. In addition to unwanted and preventable events, risks can also be favourable circumstances that have not been realized. The NAOF targets its audit work on the basis of not only the risk analysis but particularly also the legislation and its interpretation, international standards, and the decisions taken in its strategy on the targeting of audits.

The entire personnel of the NAOF has participated in identifying the risks, and the risk analysis has been made in close cooperation with the employees of the Prime Minister’s Office who are involved in foresight activities. The risk analysis supports the NAOF’s strategic goal to have societal impact through increasing the cost-effectiveness of the state’s financial management, increasing trust in the knowledge base of decision-making, and enhancing trust in open, cost-effective and sustainable operations of the Finnish central government.

The risk analysis consists of two parts:

risks to the state’s financial management, which the NAOF has assessed on the basis of its audit work;

risks to central government finances, which are based particularly on the Government’s foresight activities under the leadership of the Prime Minister’s Office.

The examination of the risks also includes monitoring the national economy and general government finances, and assessing the risks related to them using various indicators. The risk analysis is also utilized in other tasks within the NAOF, particularly in fiscal policy monitoring. Regular monitoring of compliance with fiscal policy rules and indicators help us to detect and specify the impacts of cyclical changes and other factors on general government finances. This makes it possible to detect risk areas and target fiscal policy audits using a risk-based approach.

Risks to the state’s financial management

The key risks to the state’s financial management are:

automation of financial processes,

outsourcing of functions, and

operation of the performance management system.

All of these three risk areas are relevant to efficient, service-driven public administration. In addition to the service aspect, the soundness of the financial management is also emphasized. It is basically a question of achieving balance between service ability and the other requirements set for the operations. From the audit perspective, such other requirements include economic efficiency, flawless processes, and high-quality financial information.

Automation of financial processes

Automation has significant benefits, but the identification and consideration of risks are easily left in the background, particularly in the development phase. The automation of financial processes may involve risks related to the actual process and to cost-effectiveness, legislation, or the personnel. When financial processes are automated, it is important to assess and consider the need for sufficient controls already during the preparatory phase. The processes should be genuinely revamped in order to ensure that they will increase the efficiency of operations.

Risks related to legislation can result from automation implemented without observing legislation or from legislation that presents impediments to the automation. Risks related to persons can be caused by blurred ownership and responsibility, and lack of competence.

It is also necessary to adapt audit procedures to the new automated processes, which requires development of competence and ways of working in auditing.

Outsourcing of central government functions

When central government functions are outsourced, a process or part of a process becomes an off-budget entity for instance through establishment of an unincorporated or incorporated enterprise. This weakens the NAOF’s opportunities to audit them. As regards outsourcing, it is essential to assess whether the efficiency or cost-effectiveness has improved as planned.

In the case of incorporation, the risks increase if the company to be established does not have a proper market or competition, and if its revenues are mainly generated directly by central government or by customers in compulsory tax-like contributions.

If outsourcing is implemented through procurement, the risk can be, for example, lack of procurement competence. In addition, the small size of the Finnish market can cause risks related to cost-effectiveness or interconnections. When specialist work is outsourced, risks may arise between an external actor and decision-making under the legal liability of a public official.

Questions related to the management of the whole, ownership, and knowledge can be problematic from the audit perspective.

Operation of the performance management system

The management system(s) play(s) a key role for all operations, and they are exposed to significant risks: the full capacity of the system may not be utilized, or the system may not operate as planned. In Finland, the operations of central government and its units are steered by performance management and measurements. The operations are also impacted by resource management.

Based on financial audits, monitoring of the allocation of labour costs, in particular, has clearly improved, whereas the development of effective indicators for measuring cost-effectiveness has not been as successful. There is a risk is that performance data – particularly data on economic efficiency and productivity – are utilized only to a limited extent in the management and steering of central government.

From the perspective of auditing, it is important to pay sufficient attention to the organization and development of well-functioning steering throughout the state’s financial management and the budget process.

Risks to central government finances

The key risks to central government finances are:

needs for taxation adjustments,

competence development and maintenance, and

decision-making capability.

All of these three areas are relevant to society’s capacity to operate efficiently even in the future. The risks related to central government finances were identified by analysing the vision of the future laid out by the Prime Minister’s Office. The vision of the future includes social, technological, political, ecological, and economic change factors. The NAOF has assessed the vision of the future particularly from the perspective of the future development of central government finances and the impact of audits.

Needs for taxation adjustments

Taxation is linked with all of the change factors in the vision of the future. Taxation is also among the risk areas identified by the NAOF, because audits have been clearly less frequently targeted at revenues than the use of state assets.

The new forms of globalization cause challenges to corporate taxation and, through the revolution of work, also to labour mobility and income taxation. In the social vision of the future, taxation is one of the risk areas because of the ageing population and income inequality, for example.

The fast-breaking advances in technology may reduce the amount of taxable salary income. The change in the production and use of energy may also have an impact on the amount of taxable income, as transport fuels, in particular, are a significant source of tax revenue.

Taxes have a key role in fighting the climate change and steering the development of the environment and nature. The key issue related to taxation is how to strengthen and increase the efficiency of its steering impacts.

Because taxation has extensive impacts, it is important to consider how it is linked with a planned audit topic. The links can be either direct or more difficult to perceive. Tax reliefs and income transfers or subsidies, for example, can often be alternatives to each other.

Competence maintenance and development

As the population growth is weakening, it is necessary to improve productivity in order to safeguard the conditions for wellbeing. This makes it increasingly important to maintain and develop competence. In addition, the revolution of work makes it necessary for people to learn new skills – often during their entire career.

The responsibilities related to competence are divided between municipalities, limited companies, and foundations, which causes challenges to competence-related auditing. Central government is partly directly responsible for the measures related to immigration. The responsibilities for adult education are widely dispersed, and even individuals and companies have more responsibility for it. Competence maintenance and development can be significantly impacted by steering and funding, which continue to fall within central government’s responsibility.

When competence and competence development are examined from the perspective of risks to central government finances, the examination of individual measures should always be linked to the overall context.

Decision-making capability

All of the change factors in the Government’s vision of the future are linked with high-quality decision-making. In addition to previous requirements, decision-making is faced with new, partly unexpected difficulties, which complicates the implementation of necessary decisions and especially reforms. This means significant and cumulative risks to central government finances. Audit work can improve the conditions for decision-making and impact the operation of processes, as well as the provision of information.

The change factors affecting decision-making are related, for example, to the demographic structure, the weakening dependency ratio, and the increasing inequality.

As regards the technological change factors, risks to decision-making are caused especially by cyber security and hybrid influencing. On the other hand, one of the major risks to central government’s decision-making is failure to seize the opportunities offered by technology.

The decision-making should take into account the ecological change factors, such as the climate change, the environmental situation, and sustainable use of natural resources. The decision-making is also challenged by the shift in international politics and the change in the ways of political involvement. As regards the economic change factors, the conditions of decision-making are impacted by the change in the global economy. At the same time, it is one of the change factors that has an impact on the sustainability of general government finances and the revolution of work.

From the audit perspective, the decision-making capability is often difficult to approach. Audits are targeted at the preparation of decision-making, the smoothness of the actual decision process, and the implementation of policy-making. It may be relevant to target audits at significant reforms, in particular, already in the preparatory phase. It would be important, in the preparatory phase, to coordinate future actions with other projects and measures in order to ensure coherent politics and impacts. Successful implementation of the reforms of social services and health care and social security has a key role in ensuring the sustainability of central government finances. Audits can also identify problem areas where it would be particularly important to make changes or reforms but where the decisions have not been taken, for one reason or another.

Additional information