The usability and effectiveness of audit results depend on how the audits are focused on central government and how public administration implements the recommendations contained in the audits. The financial audits conducted by the National Audit Office cover all areas of central government, while fiscal policy, compliance and performance audits focus primarily on the administrative branches bearing the main responsibility for central government finances. Most of the recommendations issued in the audits are also implemented by public administration. The National Audit Office has assumed new tasks, overhauled its organisation and launched the preparation of a new strategy.

The National Audit Office monitors the extent of its audit activities

In the period 2020–2022, the National Audit Office of Finland (NAOF) carried out between 81 and 84 audits and between 16 and 27 follow-ups each year. In the period January–August 2023, a total of 80 audits and 12 follow-ups were completed.

| 2020 | 2021 | 2022 | 1–8/2023 | |

| All audits | 82 | 84 | 81 | 80 |

| Financial audits | 68 | 70 | 69 | 71 |

| Separate audits of which | 14 | 14 | 12 | 9 |

| – Performance audits | 9 | 6 | 9 | 6 |

| – Compliance audits | 1 | 4 | 0 | 2 |

| – Fiscal policy audits | 1 | 1 | 1 | 0 |

| – Multi-type audits* | 3 | 3 | 2 | 1 |

| Follow-ups on separate audits | 18 | 27 | 16 | 12 |

* Multi-type audits are combinations of more than one audit type.

Most of the audits are financial audits, which in addition to the accounting offices in all administrative branches, also cover the final central government accounts, the Office of the President of the Republic, the Prime Minister’s Office, three off-budget government funds and two organisations under the Nordic Council of Ministers. Implementation of the recommendations issued in the financial audits of the accounting offices is monitored as part of the financial audit and for this reason, no separate follow-ups are carried out. Conclusions of the financial audits are discussed in more detail in chapter 2 of the annual report.

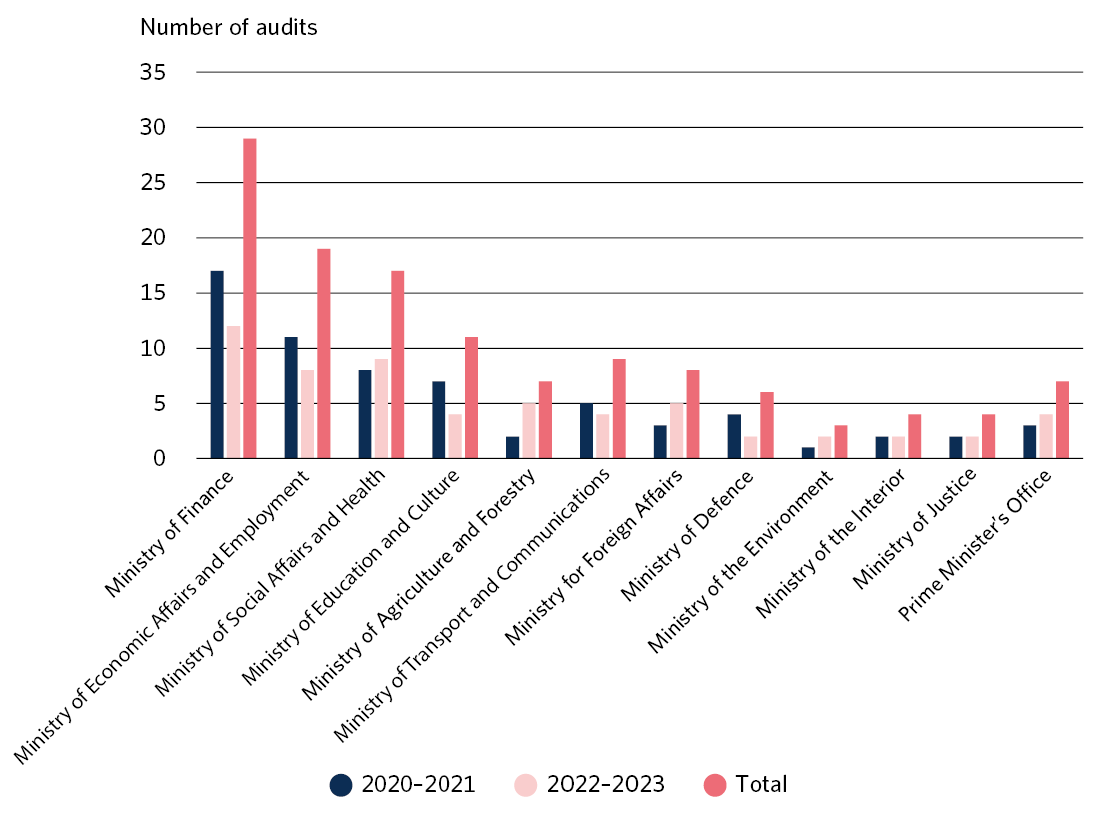

At its discretion, the National Audit Office carries out separate audits. In the period 2020–2023, about 60 per cent of them were performance audits (Table 1). The NAOF carries out separate audits comprehensively in different administrative branches, and most of them are based on the significant risks facing central government finances. Most of the separate audits are carried out in the administrative branches receiving the largest appropriations in the Budget: the Ministry of Finance, the Ministry of Economic Affairs and Employment, the Ministry of Social Affairs and Health and the Ministry of Education and Culture. Since 2020, more than 60 per cent of all separate audits have been carried out in these administrative branches (Figure 1).

The breakdown of separate audits by administrative branch varies from year to year and should therefore be monitored over a period of several years. Since 2022, more audits have been conducted in the administrative branches of the Ministry of Agriculture and Forestry, the Ministry for Foreign Affairs and the Ministry of the Environment, while there has been a reduction in the number of audits carried out in the administrative branches of the Ministry of Education and Culture and, to some extent, the Ministry of Economic Affairs and Employment, the Ministry of Defence and the Ministry of Transport and Communications.

Performance audits usually cover more than one administrative branch. This is because cooperation between administrative branches has been prioritised in the Government Programmes of recent parliamentary terms, and Government decisions are jointly implemented by administrative branches. During the annual report period (September 2022–August 2023), 13 audits were completed, eight (62 per cent) of which covered more than one administrative branch and five only one administrative branch. The follow-ups carried out during the same period covered 19 audits published between 2016 and 2021, of which nine audits covered one administrative branch and 10 audits (53 per cent) more than one administrative branch.

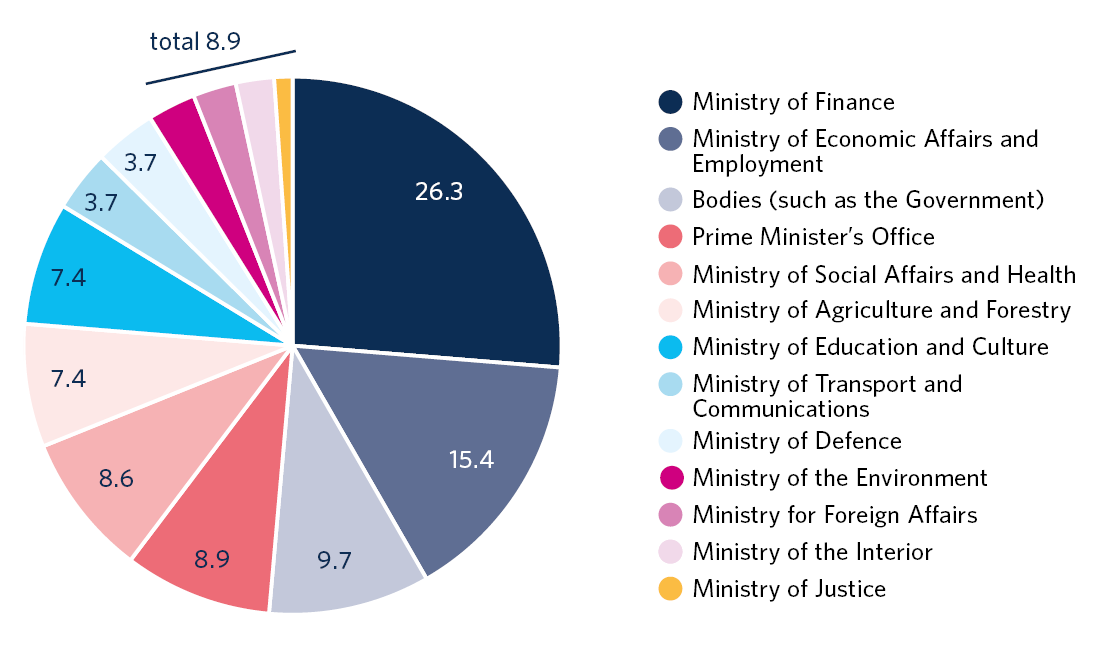

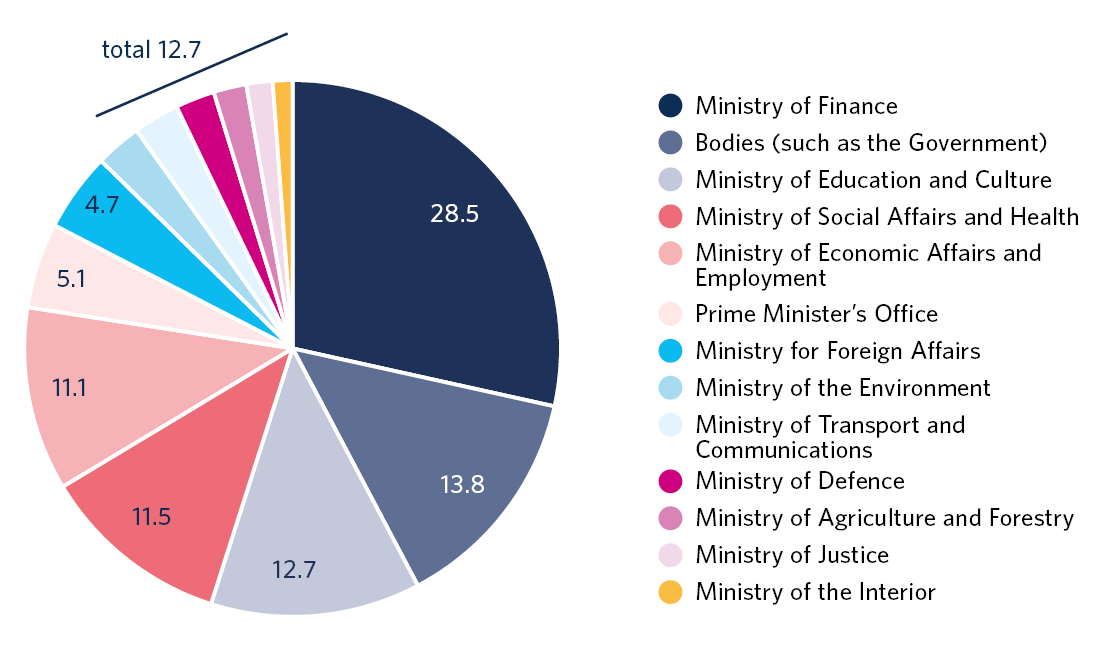

Based on its audit conclusions, the National Audit Office issues recommendations to the audited entities. In the 70 audits completed between 2014 and 2023, the highest number of recommendations was issued to the administrative branch of the Ministry of Finance. This is understandable because the focus in the audits is on risks to central government finances. The number of recommendations issued to the administrative branches of the Ministry of Economic Affairs and Employment, Ministry of Social Affairs and Health and the Ministry of Education and Culture has also been in the same proportion as the number of audits conducted in these administrative branches. (See Figures 2 and 3.)

When the number of recommendations issued to individual administrative branches in the audits completed in the periods 2014─2020 (Figure 2) and 2020─2023 (Figure 3) is compared, it can be noted that the audits conducted in the 2020s have, in relative terms, contained more recommendations jointly issued to Government or key administrative branches, whereas fewer recommendations have been issued to the Prime Minister’s Office. This trend may have partially resulted from the fact that in recent years, some of the audits have covered extensive structural reforms and policy measures outlined in the Government Programmes, and the audits have focused on the preparation of Government decisions or the implementation of legislation.

Central government actors have implemented most of the recommendations issued by the National Audit Office

In the follow-ups on the separate audits, the National Audit Office assesses the measures taken by public administration on the basis of the recommendations and conclusions issued in the audits. On average, the follow-ups are carried out about three years after the issuing of the audit report. The timing of the follow-up is determined on an audit-specific basis so that the audited entities have sufficient time to implement the recommendations.

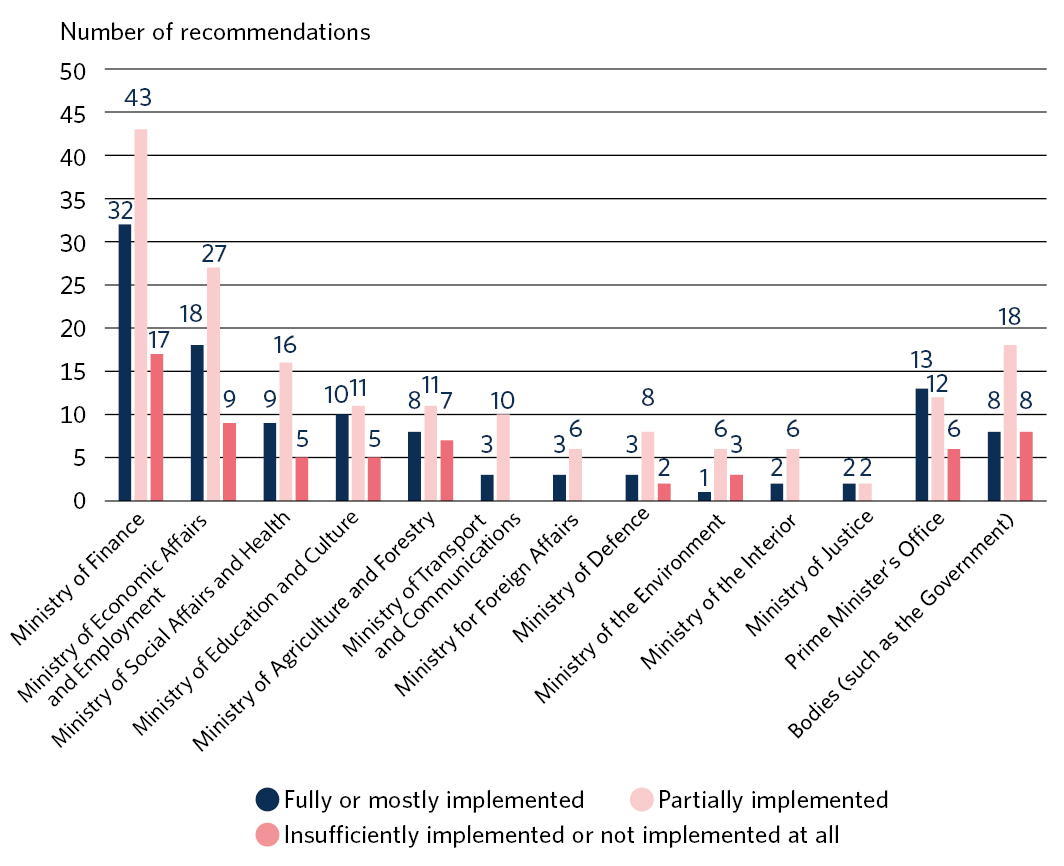

Most of the recommendations issued by the National Audit Office are implemented by the audited entities. Based on the 70 follow-ups carried out between January 2020 and June 2023, about 35 per cent of the recommendations of the audits (n=252) had been fully or mostly implemented and about 47 per cent partially implemented. About 18 per cent of the recommendations had been insufficiently implemented or had not been implemented at all (Figure 4).

Based on the follow-ups, factors impacting the implementation of the recommendations include the fact that the implementation of the recommendation is still in progress during the follow-up or that the public administration actors in question do not have the resources to implement the recommendation. Implementation of the recommendation may also have been combined with ongoing public administrative development work or the preparation and implementation of reforms or legislation. Occasionally, other legislative or administrative measures may also have been taken and as a result, the recommendation has been implemented differently or it is no longer relevant. It has been noted in the follow-ups that the implementation of the recommendations issued to more than one administrative branch or actor requires particularly close cooperation between the public administration actors concerned and extensive reforms and changes.

The National Audit Office has published viewpoints concerning the conclusions it has made in its audit, monitoring and oversight activities for the new parliamentary term

For the first time, the National Audit Office has published viewpoints on key economic and administrative policy topics that will be relevant to the achievement of balanced general and central government finances and to sustainable management of central government finances in the coming years. The purpose is to support the drafting of the Government Programme for the parliamentary term that began in April 2023. The viewpoints are based on the key findings and conclusions of the NAOF’s fiscal policy monitoring as well as the audits and follow-ups published by the NAOF during the parliamentary term 2019–2023.

The viewpoints are divided into following main themes: ‘A planned fiscal policy strengthens public finances’, ‘A clear division of responsibilities and established cooperation practices between public authorities provide support in the event of crises and disruptions’, ‘Effective benefits and public services help to secure the foundations of the welfare state’, and ‘External and internal changes challenge the central government to reform its operating practices’.

Impacts of audit activities

Financial audits cover all areas of central government. Most of the discretionary separate audits and recommendations concern the administrative branches that bear the main responsibility for central government finances. The audits and recommendations often cover matters that require cooperation across administrative boundaries. Most of the recommendations issued by the National Audit Office are implemented by public administration.

The National Audit Office published viewpoints on key economic and administrative policy topics for the new parliamentary term. The viewpoints concern themes that are relevant to the achievement of balanced general and central government finances and to sustainable management of central government finances in the coming years.

The National Audit Office overhauled its organisation in early 2023

The National Audit Office overhauled its organisation and management system during 2022. The aim was to clarify responsibilities and ensure better support for implementation of the agency’s core task. From 1 January 2023, the National Audit Office has operated as a line organisation divided into the Audit, Monitoring and Oversight, and Shared Services Units. The Audit Unit is responsible for the carrying out and quality control of the audits and prepares the opinions of the National Audit Office that concern its sector. The Monitoring and Oversight Unit is responsible for fiscal policy monitoring and audits and for the oversight of political party and election campaign funding. The unit is also responsible for the transparency register and for processing complaints and reports on irregularities submitted to the NAOF. The Shared Services Unit comprises the joint functions that support the agency’s activities and development: general administration, HR services, financial services, information management and premises services as well as communications and stakeholder coordination. All units are jointly responsible for competence development.

The National Audit Office will overhaul its strategy for the period 2024–2030 during 2023, and in this work, consideration will be given to the anticipated impacts of future change factors on the National Audit Office. The focus in the new strategy will be on the ability of the National Audit Office to perform its core tasks effectively and efficiently.

The new audit planning process, prepared during 2023, will ensure comprehensive monitoring of the operating environment and the focus of audits on essential matters. By developing audit procedures, the National Audit Office can ensure that data are extensively used in the audits. The National Audit Office has also launched a long-term development project to enhance the competence of its auditors.

At the end of 2022, fiscal policy monitoring published the fiscal policy monitoring and audit report for the 2019–2022 parliamentary term and by September 2023 two separate reports: an ex-post assessment of the accuracy of the Ministry of Finance’s budgetary forecasts and a report on the role and efficiency of automatic fiscal stabilisers in Finland. Fiscal policy monitoring has updated the business cycle heatmap and the composite indicator derived from it, which it uses in its reporting. Fiscal policy audit supports the monitoring activities so that audit findings can produce topics that are subsequently monitored as part of the monitoring work. Two fiscal policy audits are under way in 2023.

The National Audit Office is overseeing the election campaign funding of the parliamentary elections held in spring 2023 and will submit a report to Parliament on its findings in December 2023. Preparations for the combined municipal and county elections in 2025 will continue as information system development work and the drafting of new guidelines. The report on the oversight of political party funding in 2022 was submitted to Parliament in March 2023. The audits of political party organisations in 2023 will be carried out in autumn 2023.

In 2023, the National Audit Office introduced an internal whistleblowing channel to implement the provisions on the protection of persons reporting breaches of EU and national law. The function responsible for complaints and reports on irregularities aims to streamline the processing of complaints and reports on irregularities and to promote the utilisation of information received through the function in audit planning and the monitoring of the NAOF’s operating environment.

Focus in the National Audit Office’s international activities was on effective operations

The National Audit Office’s international work involves work that is binding on audit communities and discretionary international cooperation in specific cooperation forums, in accordance with the agreed priorities. The most important cooperation forums are the International Organization of Supreme Audit Institutions (INTOSAI), its European regional organisation EUROSAI, Contact Committee of the Supreme Audit Institutions of the European Union, and the Nordic cooperation network. Through international cooperation, the National Audit Office receives useful information from other countries’ audit institutions and international organisations on new methods and topical issues that it can apply in its own activities. At the same time, the National Audit Office can share its expertise with other audit institutions.

The National Audit Office is responsible for the financial audits of the European Organization for Nuclear Research (CERN), the European Southern Observatory (ESO) and the Baltic Marine Environment Protection Commission (HELCOM) as well as the financial audits of the Nordic Culture Point and the Nordic Institute for Advanced Education in Occupational Health (NIVA), which are located in Finland and operate under the auspices of the Nordic Council of Ministers.

The National Audit Office participates in the activities of international umbrella organisations at organisational, working group and network level. The National Audit Office will chair the Working Group on Environmental Auditing (WGEA) of INTOSAI until 2025. The NAOF is also in charge of the Fiscal Policy Audit Network, which operates under the auspices of the Contact Committee of the Supreme Audit Institutions of the European Union. The National Audit Office also participates in international cooperation between independent fiscal institutions for instance in the EU IFI network.

Internal activities of the National Audit Office

In 2023, the National Audit Office continued its operations as a line organisation focusing on its audit, monitoring and oversight tasks. A new strategy for the NAOF will be prepared during 2023.

Since 2022, the National Audit Office has prepared to audit the operations of wellbeing services counties as regards central government funding and the maintenance and oversight tasks of the transparency register.

Right to audit expanded to cover the wellbeing services counties, and the NAOF is preparing for its task as the registrar of the transparency register

Under the Act on Wellbeing Services Counties (611/2021) and the Act on Organising Healthcare and Social Welfare Services and Rescue Services in Uusimaa (615/2021), the National Audit Office has the right to carry out audits of the wellbeing services counties, organisations and foundations belonging to the wellbeing services county groups as well as the healthcare, social welfare and rescue services of the City of Helsinki and the organisations under the control of the City of Helsinki established for these tasks. The audits produce information on the finances and activities of the wellbeing services counties, their financial position and the special issues set jointly for the wellbeing services counties, thus ensuring that central government is able to supervise the organisation and provision of services mainly funded by central government and related to citizens’ fundamental rights. The preparation of the audit activities covering wellbeing services counties began in 2022, and the first audits were launched in 2023.

In 2022, the National Audit Office also started preparations for its new statutory task, serving as the registrar and overseer of the transparency register. Under the Transparency Register Act (98/2022) companies, associations and foundations must report their lobbying activities directed at Parliament and ministries. The purpose of the Act is to improve the transparency of lobbying directed at preparation and decision-making and, consequently, to combat inappropriate lobbying.

With the entry into force of the Transparency Register Act, the National Audit Office will become the registrar of the transparency register on 1 January 2024 and start overseeing compliance with the reporting obligation. The National Audit Office will prepare for the tasks by setting up an information system for the transparency register by the end of 2023. The National Audit Office will also prepare and publish guidelines for the actors subject to the reporting and registration obligation, organise training and events for stakeholders and arrange meetings of the advisory board established for the transparency register. The advisory board has already been appointed and it started work in May 2023.

New legislation relevant to the NAOF’s audit, monitoring and oversight activities

Section 128 of the Act on Wellbeing Services Counties (611/2021):

The National Audit Office has the right to audit the legality, appropriateness and cost-effectiveness of the activities and financial management of a wellbeing services county, the entities controlled by the county and the entities jointly controlled by counties as regards funding received from central government.

Section 23 of the Act on Organising Healthcare and Social Welfare Services and Res-cue Services in Uusimaa (615/2021):

The National Audit Office has the right to audit the legality, appropriateness and cost-effectiveness of the activities and financial management of the City of Helsinki’s healthcare, social welfare and rescue services and the entities under the control of the City of Helsinki and established for these tasks as regards the funding received from central government.

Section 9 of the Transparency Register Act (430/2023):

The National Audit Office acts as the registrar of the transparency register and over-sees compliance with the reporting obligation. For this purpose, the National Audit Office shall

guide and advice the actors subject to the reporting obligation to submit the notifi-cations specified in this Act;

check that the actors subject to the reporting obligation who have submitted the registration notification have submitted notifications of their operations;

check that the notification of permanent discontinuation of the lobbying activities and advisory activities associated with the lobbying activities or the notification of the lobbying becoming a small-scale activity submitted by the actor subject to the reporting obligation meets the requirements laid down in section 7, subsection 3;

investigate suspected negligence related to the registration notification, notification of changes in basic information, notification of permanent discontinuation of the lobbying activities and advisory activities associated with the lobbying activities or notification of the lobbying becoming a small-scale activity and the notification of operations;

if necessary, request the actor subject to the reporting obligation to submit a new notification, to supplement the notification already submitted, or to submit the report referred to in section 10, subsection 1;

maintain and develop the electronic register;

appoint the advisory board referred to in section 11;

prepare an annual report on the activities and oversight of the register;

submit a report to Parliament on the operations and oversight of the register for each parliamentary term.

The National Audit Office may request the actor subject to the reporting obligation to submit a notification laid down in this Act, correct an error or inadequacy or submit the report referred to in section 10, subsection 1. The National Audit Office may impose a conditional fine to enforce the request.