In the financial audit reports for 2022, a total of 12 central government accounting offices were issued with cautions on errors and shortcomings in the financial statements and notes to the financial statements or in the operational efficiency data. There has been a substantial increase in the number of cautions issued to the accounting offices on true and fair information in the final accounts compared to 2021 when a similar caution was issued to five accounting offices.

Under section 90 of the Constitution of Finland, the National Audit Office is responsible for auditing the management of central government finances and compliance with the Budget. Each year, the National Audit Office audits the final accounts of the central government, ministries, other government agencies obliged to submit final accounts, and three off-budget funds.

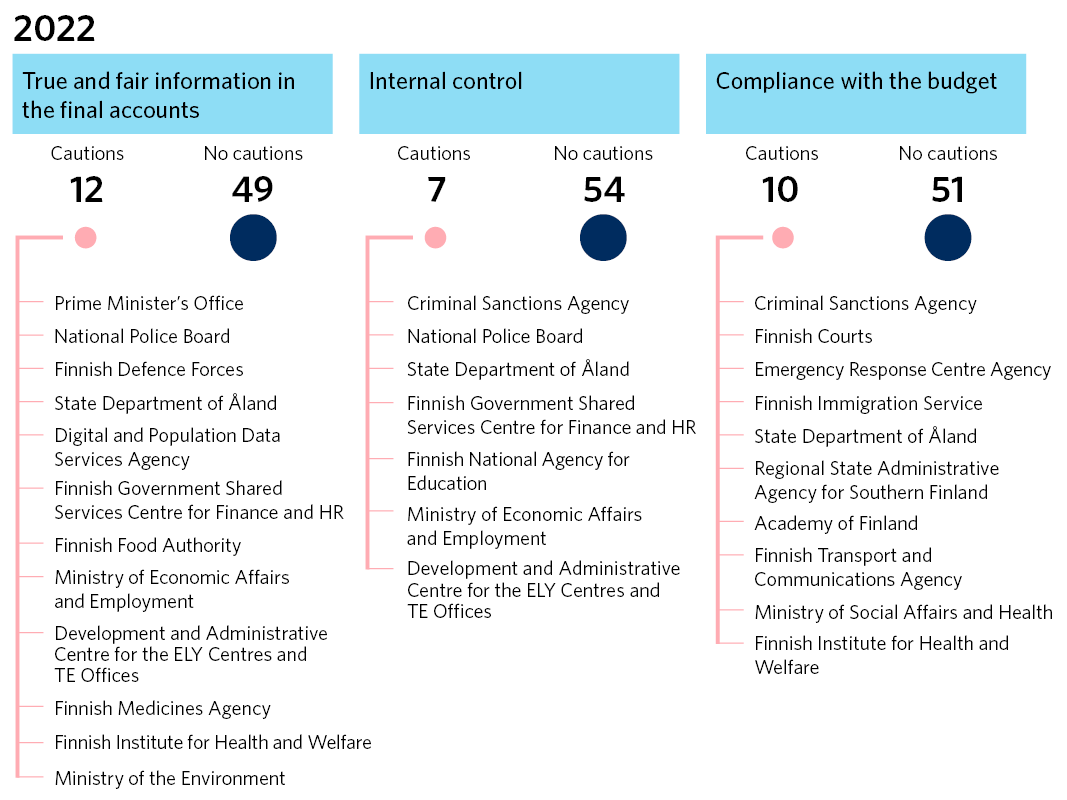

One in three accounting offices was issued with a caution on shortcomings in final accounts or financial management procedures

In the financial audit report, the National Audit Office states whether the information on final accounts and operational efficiency is true and fair, whether internal control is effective and whether the budget has been complied with. The National Audit Office issued 61 financial audit reports to central government accounting offices for 2022.1

A total of 21 (34 per cent) of the audited accounting offices received at least one caution, as material shortcomings were found in their final accounts or financial management procedures. The most significant change compared to the previous year took place in the financial statements and notes to the financial statements or in the operational efficiency data, on which cautions were issued to 12 accounting offices. Only five accounting offices received a similar caution for 2021.1

Cautions on the final accounts of the accounting offices may concern the financial statements and the notes to them or information on operational efficiency, such as cost recovery calculations on chargeable activities. Cautions on the financial statements and notes to them were issued to ten accounting offices and cautions on operational efficiency data to three accounting offices, as one accounting office received both cautions. The most important single reason for the cautions was note 12 to the financial statements (Granted state securities, state guarantees and other commitments) as four accounting offices were issued with cautions on shortcomings in them.1

In addition to the shortcomings concerning true and fair information in the final accounts, cautions were also issued in other financial audit opinion areas. Internal control cautions were issued to seven accounting offices, and a qualified opinion on regularity was issued to ten accounting offices.1 Only one accounting office (State Department of Åland) received a caution in all three opinion areas. The State Department of Åland was also obliged to report on shortcomings in good accounting practices and internal control. The reporting obligation means the obligation imposed on the management of the audited entity to report on the measures taken by the audited entity to correct the shortcomings that had prompted the caution. The reporting obligation was also imposed on the Finnish Food Authority, the Ministry of Economic Affairs and Employment and the Finnish Government Shared Services Centre for Finance and HR (Palkeet).1

In recent years, a number of accounting offices have repeatedly received a financial audit report containing a caution (modified opinion). Three accounting offices have received a caution in at least seven successive years. These are the Development and Administrative Centre for the ELY Centres and TE Offices, Palkeet, and the Ministry of Economic Affairs and Employment.1

Fewer cautions on regularity were issued – however, procedures violating the budget are still common

The National Audit Office issues a qualified opinion on regularity to an accounting office if the budget or the key budget provisions have not been complied with in all respects. A qualified opinion on regularity usually concerns one area or procedure of financial management and thus, receiving it does not mean that the government agency’s or central government’s finances have been managed unlawfully or that government funds have been misused. However, a qualified opinion on regularity should always be considered to be a serious matter with regard to the financial management of the government agency in question.1

Ten of the 61 financial audit reports issued by the National Audit Office contained a qualified opinion on regularity,1 and the number of accounting offices issued with a caution on regularity remained more or less unchanged in the period 2020–2022: 11 accounting offices in 2020, 9 accounting offices in 2021 and 10 accounting offices in 2022. The total number of the cautions on regularity may be higher because one accounting office may receive one or more cautions on regularity on a specific matter. In 2022, all qualified opinions on regularity contained only one caution on regularity and thus their total number was ten. In 2020 and 2021, a number of accounting offices received more than one caution on regularity and thus their total number was higher than in 2022: 14 cautions on regularity for 2020 and 13 cautions on regularity for 2021.1

The incorrect procedure prompting the opinion on regularity may be related to compliance with the budget or internal control. In recent years, most of the cautions on regularity concerning compliance with the budget have been issued because the accounting office has used an appropriation in the wrong budget year or for a purpose to which it was not allocated in the budget. Cautions on regularity concerning internal control may also be based on non-compliance with other budget provisions. In the final accounts for 2022, the most common reason for the caution on regularity was that budget expenditure had been allocated to the wrong budget year in violation of the budget and section 5a of the State Budget Decree (1243/1992). Moreover, in all cases, in addition to the allocation error, the procedure had also extended the use of the appropriation in violation of section 7 of the State Budget Act (423/1988). This prompted the National Audit Office to issue a caution to four accounting offices.1

Qualified opinions on regularity are fairly evenly distributed between accounting offices in different administrative branches. Based on the financial audit reports for 2022, two accounting offices in the administrative branches of the Ministry of Justice, the Ministry of the Interior, the Ministry of Finance and the Ministry of Social Affairs and Health received a qualified opinion on regularity. In the five-year time series, the only administrative branches where accounting offices have not received any qualified opinions on regularity are the Ministry of Agriculture and Forestry and the Ministry of the Environment. 1

Key findings of the National Audit Office on the financial audits of central government accounting offices in 2022

Compared to 2021, there was an increase in the number of cautions concerning the financial statements and notes to the financial statements or the operational efficiency data of the accounting offices.

Three accounting offices have received a financial audit report containing a caution (modified opinion) in at least seven successive years.

The number of accounting offices receiving a caution on regularity remained almost unchanged between 2020 and 2022.

Progress has been achieved in ensuring uniformity of the budget – the development work should continue

It was noted in the audit of the uniformity of the budget (11/2020) that the budget drafting procedures used between 2015 and 2020 were not unified, and that the guidelines for drafting the budget had not been fully complied with. The National Audit Office recommended that the controls related to budget preparation and the processing of budget proposals should be improved and the breakdown of the budget accounts simplified. The National Audit Office carried out follow-ups on the audit in two phases (in 2021 and 2022). Based on the second phase of the follow-up, such measures as better controls and fewer mixed items have enhanced budget uniformity. In addition, proposals contrary to the budget preparation regulation have also been addressed more vigorously than in the past. The development work should continue. Based on the follow-up, the class and item structure of the main titles have not been subject to any major development measures. Moreover, the account breakdown has not been simplified, which is also the result of the new items reserved for the Recovery and Resilience Facility. In the future, the National Audit Office will assess the appropriateness and uniformity of budget procedures as part of the annual financial audit process.2

Shortcomings in support and grants to non-profit organisations have been addressed by public administration

A number of irregular procedures and deficiencies in internal control were identified in the audit of support granted to non-profit organisations (11/2019). Shortcomings were identified in such areas as the payment and supervision of grants and their advances, publication of calls, rules and conditions of grants, and the submission of information to the Cabinet Finance Committee. Deficiencies were identified in the administrative branches of the Ministry of Agriculture and Forestry, Ministry of Education and Culture, Ministry of Social Affairs and Health and Ministry of Economic Affairs and Employment. It was also noted in the audit that the legislation on grants should be updated. In particular, the legislation concerning the Finnish Institute of Occupational Health was in many respects outdated. Based on the follow-up, most of the audited entities had taken corrective action. The National Audit Office will continue the monitoring in connection with financial audits.3

No shortcomings were identified in related party relationships and transactions in central government

From the perspective of transparency, legality and the principles of good governance, it is important that the transactions with related parties of central government are in accordance with the law and that the internal control procedures related to them are adequate and appropriate. It was examined in the audit whether errors or misuse can be identified in central government related party transactions and whether internal control related to the processing of the related party transactions is appropriately organised.

Based on the audit, the senior public officials of central government accounting offices had connections to a total of 477 different organisations, 236 of which were associations, 157 companies and 84 foundations. About a quarter of the organisations had carried out transactions with central government actors. No shortcomings were identified in the audited related party transactions between central government and its related party persons and organisations. No material shortcomings were identified in the information content of the declarations of interests of the senior management, compliance with the declaration obligation or the organisation of the monitoring of the declarations. At the same time, it is not possible to transparently identify from the final accounts of the central government accounting offices whether an accounting office has had transactions with parties that could be considered related parties of the accounting office in question.4

There is room for improvement in the control of self-assessed taxes

Self-assessed taxes include value added tax and excise duties. The taxpayer is responsible for calculating, reporting and paying the self-assessed taxes. In the 2022 Budget, self-assessed taxes accounted for about 65 per cent (EUR 29 billion) of all central government tax revenue. The Act on the Tax Procedures for Self-Assessed Taxes (768/2016) entered into force in 2017. Based on the audit, the procedures for self-assessed taxes have been harmonised so that the act contains general provisions on the procedures as well as provisions on certain harmonised procedures, such as tax periods, tax returns, payment and imposition of taxes, penalties and appeals.5

Legislation-based implementation clarifies the taxation procedures for self-assessed taxes. Improving administrative efficiency was also one of the objectives of the reform. The purpose of both legislation and practical taxation activities has been to minimise the number of tax decisions, especially in value-added taxation. Based on the audit, the line between an authority-initiated and a taxpayer-initiated taxation change is vague. For many years, the Finnish Tax Administration focused on controlling large companies and companies with international operations. However, this goal was abandoned when the emphasis shifted to the proactive guidance procedures applied by the Large Taxpayers’ Office. Proactive guidance is considered an effective way of targeting guidance to large customer groups, even though clear indicators are missing.5

Based on the audit, the control of VAT returns per tax period has decreased significantly, and the control is only loosely based on selection, which is a well-established way of channelling transactions to processing mainly on a risk basis. The provision on selection allows for a different degree of examination in automated taxation. The National Audit Office is of the view that a procedure in which only some of the VAT returns selected with the same control rules are controlled does not promote the achievement of the objectives of consistent taxation. The risk of the procedure is that the guarantees of good governance are not realised and the legal protection of the taxpayer is endangered.

It is stated in the audit that the procedures for tax control and guidance of taxpayers vary, and the Act on Tax Assessment only contains provisions on the principles and practices of a small number of guidance and control methods used by the Finnish Tax Administration. Moreover, the handprint of value added tax control presented as an indicator of the effectiveness of value added tax control in the final accounts of the Finnish Tax Administration gives an essentially incorrect picture of the effectiveness of the control.5

Recommendations of the National Audit Office on the control of self-assessed taxes

It should be assessed how the prerequisites for the control of self-assessed taxes, particularly value added taxes, and the reliability of its indicators could be improved, also taking into account the tax control duties of Finnish Customs in excise taxation. The need to regulate new methods of guidance and control by the Finnish Tax Administra-tion should also be assessed, and legislation should be developed so that it would boost the efficiency of the taxation process while promoting the correctness of taxation and treating taxpayers equally.5