Ensuring that the functions for which central government is responsible can continue without interruptions in all situations is a key task of the government. This requires an active risk management policy at different levels of central government and in state-controlled companies. The focus in the risk and continuity management of central government is on safeguarding the functions that are important for the functioning of central government and society at large as well as on adequate monitoring of the risks to central government finances, government guarantees and liabilities and sufficient access to information on them. Proper functioning of state ownership steering plays a significant role in the latter area.

Systematic and proactive risk and continuity management ensures the functioning of central government in all situations

The purpose of risk and continuity management in central government is to safeguard the continuity of the functions that are government responsibilities in normal conditions, during disruptions occurring in normal conditions and in exceptional circumstances.

It was noted in the audit (20/2018) carried out in 2018, which discussed risk management in central government and ensuring the continuity of the government agencies’ operations during disruptions occurring in normal conditions that there is room for improvement in the plans of government agencies to ensure the continuity of their operations. According to the audit findings, centralisation of internal services of central government and new networked operating models require the management of continuity risks across agencies’ boundaries. Based on the audit follow-up, risk and continuity management have been developed in the manner required by Parliament. In 2018, Parliament called for the Government to define risk management procedures at different levels of central government by the end of 2020. In accordance with the proposal of the working group that prepared the matter, a risk management division was established under the Advisory Board on Internal Control and Risk Management. The task of the division is to prepare a government resolution on Government’s risk management policy and to coordinate risk management at Government level. The first term of the division will end on 31 December 2024. The Government Financial Controller’s Function has also received additional resources for its risk management activities on a temporary basis. With the help of the additional resources, a glossary of concepts explaining central government’s financial risks and liabilities and the steering of implementation will be prepared, and the national framework and norms for risk management will be developed.1

Based on a survey conducted by the Advisory Board on Internal Control and Risk Management in summer 2019, government agencies, state funds and unincorporated state enterprises have produced fairly accurate definitions of risk management principles. A large proportion of government agencies had also prepared separate risk management policies and risk management action plans. There are also plans to include the perspective of risk management in the performance management processes of individual ministries. Because of the security situation, particular attention has been paid to the development of the risk management and continuity of the services provided by the Government ICT Centre Valtori.1

Supervision of the strategic interests of ownership steering in state-owned companies is largely based on the trust between the owner and the company’s management

At the end of 2022, the state had holdings in 69 companies. In 2022, the turnover of the companies owned by the state directly or through the investment company Solidium Oy totalled about EUR 144 billion, and the companies employed about 300,000 persons.

In strategic-interest companies, state ownership is based on both economic investor interest and on strategic interest that is essential or critical for the functioning of society. In these companies, the strategic interest concerns such matters as national defence, security of supply, maintaining infrastructure or ensuring that the obligation to provide basic services is met. There are differences between companies concerning the extent to which the strategic interest is part of their operations. The State of Finland currently has controlling interest over 17 strategic-interest limited liability companies. The ownership steering of fifteen of these companies is the responsibility of the Ownership Steering Department of the Prime Minister’s Office, while two of the companies are steered by the Ministry of Finance. The Ownership Steering Department is responsible for the companies’ strategic interests, which it prepares in cooperation with the line ministries.

The National Audit Office has audited the functioning of the ownership steering of strategic-interest companies. It was concluded in the audit that for the functioning of society, the most significant risks related to the strategic interest of the companies should be identified and assessed at government level as part of the management of administrative and financial risks pertaining to central government.2

Based on the audit, the Ownership Steering Department of the Prime Minister’s Office has in many ways worked to ensure that it receives sufficient information on the state of the companies and their compliance with the government resolution on ownership policy. The department has ensured that the companies have risk management processes and analysed the risks and opportunities of the companies. However, the department does not comment on the companies’ risk level, risk-taking capacity or the functioning of their risk management practices. In its capacity as owner, the central government discusses risks with the companies and assesses their risk levels in relation to the companies’ financial capacity but does not participate in the companies’ risk management process. Through the members appointed to the board of directors, central government can influence the companies’ risk management policies and ensure that they have all necessary risk-management functions in place. In fact, ownership strategic work is largely based on confidential communications between the owner (central government) and the companies’ management and representatives. For this reason, it is difficult to assess the impact of ownership steering on the companies’ performance.2

The government resolution on ownership policy should be specified with regard to the risks to the government’s strategic interests

The owner exercises direct influence to ensure that the decisions of the general meeting are in accordance with its interests. In recent years, the general meeting guidelines issued to the companies each year by the Ownership Steering Department have emphasised the importance of comprehensive and up-to-date risk management. The auditor is expected to provide an overview of the material observations related to the financial audit, which can be considered to include any findings concerning material shortcomings in risk management. This was stated for the first time in the guidelines issued in autumn 2021. In the guidelines issued in autumn 2022, companies are also requested to present an overview of their risks and risk management at the general meeting as part of the review of the financial statements. The Ownership Steering Department may also make enquiries to request situational awareness information from companies or groups of companies on how the threat and realisation of major international risks affect the companies’ business operations. In the view of the National Audit Office, it may be necessary for the government owner to intervene in the financing and risk management of the companies more extensively and in a more binding manner by issuing guidelines in significant and problematic risk situations.2

It is clearly stated in the government resolution on ownership policy that a company’s board of directors and management must bring essential matters to the owner’s attention. On the basis of the audit, it should also be stated in the government resolution that the risks to the government’s strategic interests should, if necessary, be discussed between the company, the Ownership Steering Department and the line ministry. It was previously stated in the government resolution that the strategic interests of the government should not be endangered by the actions of the state owner or by the decisions taken by the company’s bodies. The National Audit Office recommends that this statement or a similar entry should be reinstated in the government resolution.2

The Ownership Steering Department of the Prime Minister’s Office has launched an update of the government resolution on ownership policy. As part of the work, the strategic interests and special assignments of all state-owned companies will also be updated. Priorities in the development of state ownership steering during the parliamentary term 2023–2027 are active ownership, accountability, comprehensive security and centralisation of ownership steering.

There has been an increase in government guarantees granted to Finnfund and the interest income received by the company since 2014, while at the same time, Finnfund’s sales profits and dividend income have decreased

Finnfund (Finnish Fund for Industrial Cooperation Ltd) is a special assignment company under the ownership steering of the Ministry for Foreign Affairs. It is almost wholly owned by the state, and its purpose is to promote economic and social development in developing countries by offering companies operating in them equity risk financing, long-term investment loans, mezzanine financing and special expertise in investments in developing countries.

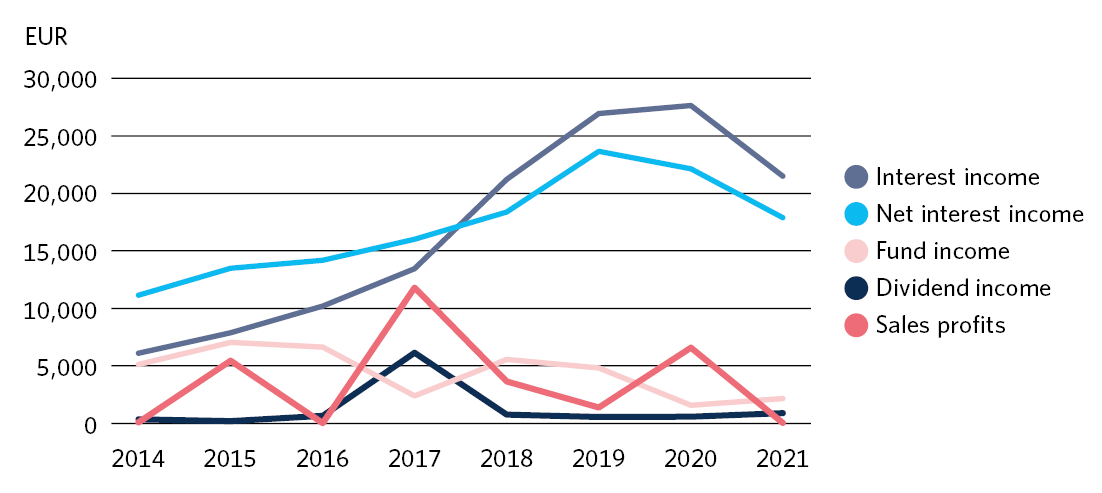

Finnfund has made between 20 and 30 new investments each year with a total value of between EUR 200 and 250 million. The loans granted by the company accounted for about 40 per cent of the company’s investment portfolio in 2020. For this reason, interest income accounts for a significant proportion of the company’s financial income. The company’s interest income increased more than five-fold between 2014 and 2020, while its sales profits and dividend income decreased during the same period (Figure 1). At the end of 2021, the balance sheet value of Finnfund’s investment assets totalled EUR 657 million. Finnfund’s tied equity and share portfolio have been boosted by the increases in share capital made by the government with a share issue subject to a charge. In 2020, the government boosted Finnfund’s share capital by an extra EUR 50 million in addition to an annual investment of EUR 10 million.3

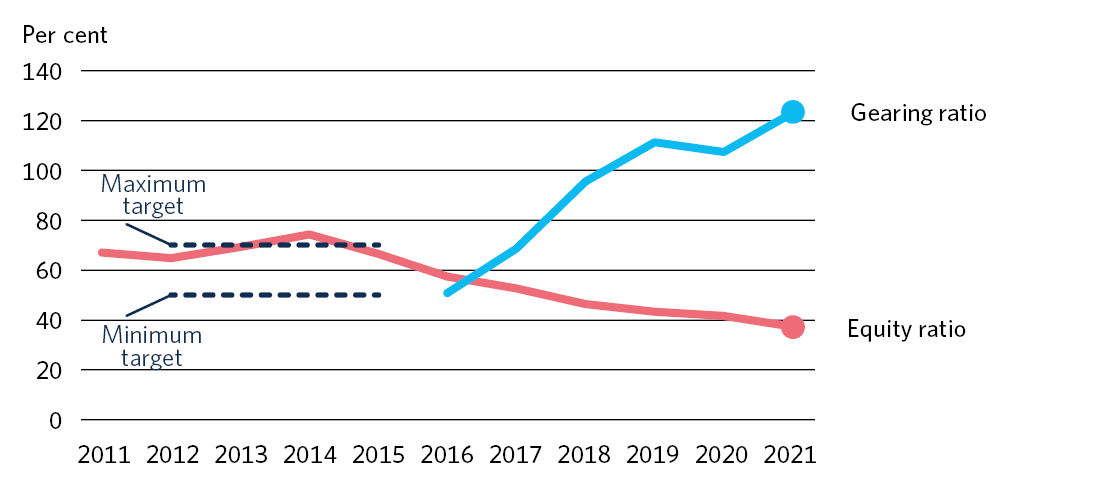

The government guarantees granted to Finnfund as part of contingent liabilities account for only 1.4 per cent of all government guarantees. However, government guarantees increased by about EUR 77 million between 2017 and 2021. Since 2015, the State of Finland has financed Finnfund with two long-term convertible bonds. In 2016, Finnfund signed an agreement with the State of Finland on a EUR 130 million subordinated convertible bond with a loan period of 40 years. The government has the right to convert the loan, in whole or in part, into Finnfund’s shares. At the end of 2019, Finnfund agreed with the government on a second convertible bond, which has a value of EUR 210 million. The terms of the loan were otherwise the same as in 2016 with the exception that the loan is automatically converted into the company’s share capital in its entirety if the company’s equity ratio drops to 10 per cent. Between 2014 and 2021, Finnfund’s equity ratio decreased steadily from about 70 to 40 per cent (Figure 2).

Both Finnfund bonds have been treated in the Budget as financial investments outside central government spending limits because the company’s investments are expected to retain their value and return to the government with interest. The substantial debts accumulated by the company may also lead to a significant decrease in equity ratio. Based on the audit, loan financing outside central government spending limits impacts central government finances but it is not subject to the restrictions set by the expenditure objective. However, the mechanism may lead to a situation where instead of equity financing, loan financing is favoured in Finnfund’s financing.3

The primary objective of the companies financed by Finnfund is to generate financial returns. The yield target set for Finnfund’s five-year average has been more than 2 per cent since 2014, and before that year, the target was even higher. Based on the audit, Finnfund has failed to achieve its financial return targets since 2011. Finnfund has expanded its operations and further expansion is planned. For this reason, attention should be paid to Finnfund’s investment activities and the criteria on which they are based.3

Finnfund’s ownership steering has not encouraged the company to produce more specific development impact targets

Development impacts are expected to arise when the requirements set for Finnfund’s investment objects concerning location, sector and sustainability are realised in the financed projects and when the investments are of sufficient size. However, based on the audit, Finnfund’s ownership steering has not required the companies to present any concrete development impact targets. Furthermore, Finnfund has not prepared any description of its development impact targets as its strategic focus has been on how to promote development in the countries where the investments are made. Finnfund has also developed instruments for ex-ante assessment and measurement of project-specific impacts. In the future, however, it should prepare clear development impact targets for its activities, on the basis of which the assessment and monitoring of project-specific development impacts can be improved.3

The objectives set by the state ownership steering encourage Finnfund to invest in high-risk projects. The main purpose of the special risk financing instrument has been to encourage Finnfund to invest in higher-risk projects with significant impacts. With the instrument, the government has pledged to partially compensate Finnfund for its investment losses. For this reason, the ownership steering should take into account the financial and other risks incurred by the government as a result of Finnfund’s activities and any liabilities arising from them (including hidden ones). However, based on the audit, Finnfund’s ownership steering has not produced any assessment of to what extent the government can increase its financing in Finnfund.3

Finnfund uses a systematic investment process in which investment destinations are assessed from the perspective of financial and other risks. Finnfund’s development impacts should play a more important role when project decisions are made, and when selecting investment destinations, Finnfund should assess the risks and potential development impacts and the relationship between them. However, the projects that Finnfund will select for its investments are not necessarily known when fund investment decisions are made.

Finnfund receives most of the investment proposals from a network of established operators, which may be inaccessible to local companies operating in the developing countries. Finnfund monitors the risks associated with its investment activities at project-specific basis and at portfolio level. To diversify and manage risks, risk management has set a variety of different target distributions and restrictions for Finnfund’s investment portfolio. Finnfund finances projects using different investment instruments that differ according to the risks they involve and Finnfund’s participation in the activities of the investment destination. Finnfund is able to participate in the operations of companies funded with a loan instrument less extensively than in the operations of companies funded by equity financing.3

Recommendations of the National Audit Office concerning state ownership steering

In the ownership steering of strategic-interest companies, the government should continue the identification of risks arising from the endangering of the companies’ business continuity and take further measures to develop methods to obtain and provide additional information on risk management. It should also be assessed whether corporate economic analyses could include periodic analyses of the level of the company’s risk management system.2

The Ownership Steering Department of the Prime Minister’s Office should take into account the views of the ministries steering the companies when the ownership strategic interest of the companies is determined or updated.2

In Finnfund’s ownership steering, more attention should be paid to the financial and other risks and potential liabilities that Finnfund’s operations may cause to the state. The ownership steering should also determine how much financing can be granted to Finnfund and which instruments can be used for this purpose.3

Joining international organisations may involve government guarantees and liabilities

By concluding treaties with international organisations, the member states undertake to accept responsibility for existing commitments and liabilities. For this reason, before joining international organisations, Finland should identify the financial impacts of the accession and determine whether, as part of the accession, it must grant government guarantees or whether the decision to join the organisation requires parliamentary approval. The Government proposal must present the liabilities or financial impacts arising from the accession and their scope in sufficient detail.

According to the follow-up on the compliance audit of financial liabilities of the government in international organisations (3/2018), the need for better identification of and reporting on government liabilities has been generally recognised in such projects as the project to develop central government group accounting. However, information on the memberships in international organisations and the related financing contributions is not collected in a centralised manner as separate monitoring of such matters has not been considered necessary. Monitoring of international memberships and the related financing contributions should therefore be part of the day-to-day development of financial management processes and systems.4

Risks arising from the interest subsidy loans granted by the Housing Finance and Development Centre of Finland (ARA) should be assessed in more detail

The Housing Finance and Development Centre of Finland (ARA) provides its individual and corporate customers with government grants, subsidies and guarantees for housing and housing construction. ARA’s task is to ensure through steering and monitoring that central government support is channelled to residents and that rental housing corporations comply with the provisions, regulations and instructions concerning state-subsidised housing construction and do not generate more income for their owners than is permitted by law. The government supports the construction, repair and acquisition of affordable rental and right-of-occupancy housing with long-term interest subsidy loans guaranteed by it. The government pays interest subsidies for the loans when the interest exceeds the basic deductible interest laid down in the Decree on Interest Subsidies. Interest-subsidised dwellings are subject to a cost rent, which means that tenants may be charged rent up to the amount required to cover the financing costs of the dwelling and the maintenance costs arising from property maintenance. ARA monitors the manner in which the cost rents are determined. At the end of 2021, ARA dwellings that are supervised by ARA and that are in use and subject to restrictions totalled about 400,000. More than half of them were ordinary rental dwellings. In 2021, ARA used 97 per cent (EUR 1.75 billion) of its interest subsidy authorisation.

Based on the audit of ARA’s operations, the use of subsidised loans is hampered by the long maturity and the backloading of the repayment programme. In the future, Municipality Finance Plc may be the only provider of financing for long-term subsidised loans, as financial institutions are reluctant to fund interest subsidy loans. Guarantee liability risks of the government are largely determined in the credit granting stage, which the State Treasury is unable to influence even though it plays a key role in the risk management, financial rehabilitation measures and insolvency procedure of ARA’s housing stock.5

Based on the audit, ARA has comprehensive control over the revenues collected by corporate customers but shortcomings were identified in the guidelines and monitoring of compliance with the principle of non-profit-making and cost rents and maintenance charges. The shortcomings in supervision arise from insufficient steering and monitoring resources, problems with information systems, inadequate guidelines for monitoring and inspections as well as the absence of systematic monitoring. The National Audit Office recommends that these shortcomings should be corrected.5

In March 2023, the Government approved an amendment to the Decree on Interest Subsidies to improve the terms and conditions of the long-term interest subsidy model for housing construction. Prior to the amendment, the basic deductible interest on rental housing construction was temporarily reduced to 1.7 per cent until 31 December 2023. Under the amendment to the Decree on Interest Subsidies, the basic deductible for interest on the interest subsidy loan paid by the borrower will be set at 2.3 per cent from the beginning of 2024 (the rate had previously been 2.5 per cent). The interest subsidy payment period will also be extended to cover the entire loan period. Increasing the interest subsidy will ease the pressures to increase cost rents and maintenance charges and it will thus improve the position of residents.

National Audit Office’s recommendations on supporting housing and housing construction

Cooperation and sharing of information between ARA and the State Treasury should be improved so that in the future the State Treasury would be able to participate in the assessment of the eligibility of high-risk funding applicants and receive up-to-date information on the criteria for granting ARA funding.5

When funding is granted, particular attention should be paid to the risks arising from the combined effect of permanent restrictions on right-of-occupancy housing and predicted migration.5

ARA should monitor the proceeds entered as revenue by corporate customers more effectively.5

In the strategic capability projects of the Finnish Defence Forces, it is important to ensure cost transparency and external quality assurance

The audit the National Audit Office completed in 2020 of the Finnish Defence Forces’ Squadron 2020 and HX fighter projects produced information on the long-term cost impacts and risks of the projects. The National Audit Office has followed up the projects continuously because they have a significant impact on central government finances. In spring 2022, after the decision to purchase the fighters, the HX project was renamed the F-35 project. The first of the new F-35 multi-role fighters are expected to arrive in Finland in 2026. The Squadron 2020 project of the Finnish Navy is now two years behind schedule. The construction of the first hull should start at the RMC shipyard in Rauma at the beginning of 2024. External quality assurance has been one of the instruments used to ensure the progress of the projects. Based on the follow-up, risks have been identified and assessed thoroughly in the projects. However, both projects involve significant financial and other risks on which the projects can only have limited influence. It is important to ensure that the costs arising from the projects are transparent and that decision-makers and society are kept adequately up to date on the progress of the projects.6

The chapter is based on the following audits and follow-ups:

Finnfund’s investment activities and risk management (3/2023)

Follow-up report of 29 December 2022 on the audit Expenses of and funding for the strategic capability projects of the Finnish Defence Forces (8/2020) (in Finnish). The follow-up report is confidential (Restricted, TL IV, section 24 (1)(10) of the Act on the Openness of Government Activities (621/1999)).